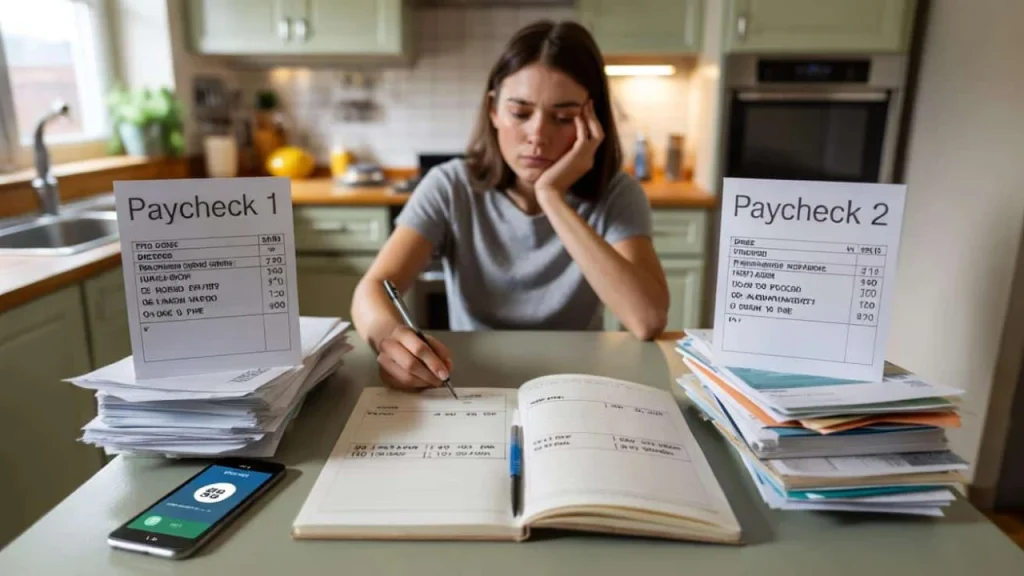

Sarah stared at her phone screen in disbelief. The grocery store checkout total was $127, but her checking account showed just $89. Behind her, a line of impatient shoppers grew longer while she frantically calculated whether she could cover the difference with her credit card without maxing it out. This wasn’t supposed to happen again.

She had a steady job, paid her bills on time, and wasn’t splurging on designer anything. Yet here she was, three weeks into the month, scrambling to buy basic groceries. The math should have worked. On paper, her income covered all her expenses with money left over. But reality kept proving her budget wrong, creating a mysterious $700 gap that appeared like clockwork every month.

The answer wasn’t cutting expenses or finding more income. It was something much simpler and more frustrating: she was planning her money at completely the wrong time.

Why calendar-based budgeting creates phantom budget gaps

Most people budget the way they were taught – from the first to the last day of each month. It seems logical. Rent is due on the 1st, credit cards on the 15th, and paychecks arrive twice monthly. Everything should align perfectly in a neat 30-day cycle.

- My plants were dying on cloudy days until I discovered wind steals water faster than blazing sun

- Millions of families scramble as inheritance law changes hit February deadline

- Peru’s 5,200 mysterious rock holes finally explained—and it wasn’t what archaeologists expected

- These 8 parenting habits secretly destroy your child’s respect—and most parents don’t even realize it

- Your daily walking route is quietly rewiring your brain’s response to unexpected changes

- House of the Dragon returns in two weeks and fans are already bracing for George R.R. Martin’s next heartbreak

The problem is that paychecks and bills rarely sync up with calendar months. When you get paid on the 1st and 15th, your first paycheck needs to stretch until mid-month, while your second paycheck has to last until the next month’s first payday. That’s not two equal 15-day periods – it’s two completely different financial challenges.

“Most budget failures happen because people plan in months but live in pay periods,” explains financial planner Maria Rodriguez, who has helped hundreds of clients solve similar timing issues. “The calendar doesn’t care about your cash flow.”

This mismatch creates what experts call “phantom debt” – money you think you have but actually don’t. Your monthly budget might show $200 left for groceries, but if most of your bills hit right after your first paycheck, that money was already spent before you realized it.

The pay-period budgeting method that closes the gap

The solution involves abandoning monthly budgets entirely and switching to paycheck-based planning. Instead of budgeting from January 1st to January 31st, you budget from paycheck to paycheck, creating two separate mini-budgets that reflect your actual cash flow.

Here’s how the timing shift works in practice:

- Map your actual pay dates – Write down exactly when money hits your account, not approximate dates

- List bills by pay period – Group expenses by which paycheck will actually cover them

- Split flexible expenses – Divide groceries, gas, and entertainment across both pay periods

- Account for uneven periods – The second pay period often stretches longer than the first

- Build separate emergency cushions – Each pay period needs its own buffer for unexpected costs

| Old Method (Monthly) | New Method (Pay Period) |

|---|---|

| Budget: Jan 1-31 | Budget 1: Jan 1-15, Budget 2: Jan 16-31 |

| All bills in one plan | Bills split by actual due dates |

| $2,000 grocery budget | $120 first period, $130 second period |

| Monthly emergency fund | Separate buffers for each paycheck |

| One big financial picture | Two realistic mini-budgets |

“When I switched to paycheck budgeting, my $700 gap disappeared overnight,” says budget coach Jennifer Kim. “Suddenly I could see exactly which bills were creating the cash flow problem.”

What changes when you time your budget planning correctly

The shift from monthly to pay-period budgeting affects more than just your bank balance. It fundamentally changes how you think about money and spending decisions.

First, you stop making financial promises you can’t keep. When your rent, car payment, and utilities all cluster around your first paycheck, you can see immediately that there’s no room for a weekend shopping trip. Your budget becomes honest about what’s actually possible.

Second, you eliminate the feast-or-famine cycle that destroys most budgets. Instead of feeling rich on payday and broke by week three, your spending stays consistent because each pay period has its own realistic limits.

The psychological impact is huge. “Timing-based budgeting removes the guilt and mystery from money management,” explains behavioral economist Dr. Ryan Peters. “When you know exactly which paycheck covers which expenses, every purchase becomes a clear yes or no decision.”

Many people discover that their budget gap was never about overspending – it was about mis-timing their spending. Bills that seemed manageable in a monthly view become obvious cash flow problems when viewed by pay period.

This method also reveals hidden opportunities for improvement. You might realize that moving your phone bill from the 25th to the 5th would balance your pay periods better, or that your second paycheck consistently has more breathing room for savings.

The most important change is that your budget starts reflecting reality instead of wishful thinking. When your planning timeline matches your actual money flow, those mysterious budget gaps stop being mysterious. They become predictable, manageable, and ultimately fixable through better timing rather than painful cuts.

FAQs

How do I handle months with three paychecks if I’m paid bi-weekly?

Those become bonus months where you can catch up on savings or pay down debt, since your bills are already covered by your regular two-paycheck budget.

What if my bills don’t align well with my pay periods?

Contact your service providers to change due dates. Most companies will adjust billing cycles to help you manage cash flow better.

Should I still track monthly expenses for tax purposes?

Yes, but keep separate records. Use pay-period budgets for daily management and monthly totals for taxes and long-term planning.

How do I handle irregular expenses like car repairs?

Build a small buffer into each pay period budget, and keep a separate irregular expense fund that you contribute to with each paycheck.

What if my income varies each pay period?

Base your budget on your lowest typical paycheck, and treat higher pay periods as opportunities to build savings or pay extra on debt.

How long does it take to see results from this timing change?

Most people notice immediate improvement in their cash flow awareness, with the actual budget gap closing within 2-3 pay periods as spending aligns with the new system.